The impact of upfront fees: structuring, open products and amortization

The 'upfront' refers to the fee amount paid to the distributor(s) and sub-distributor(s) for marketing a structured product.

Distribution is considered direct when the issuer directly interacts with the Financial Advisor of the final investor. In this case, the Financial Advisor acts as the distributor.

Distribution is considered intermediated when the issuer interacts with a broker or a platform, which then communicates with the Financial Advisor of the final investor. Here, the broker acts as the distributor, and the Financial Advisor as the sub-distributor.

🛠 Structuring

When designing a structured product, the level of upfront requested by the distributor will impact one or more other features, such as the coupon level, the capital protection barrier, or the maturity.

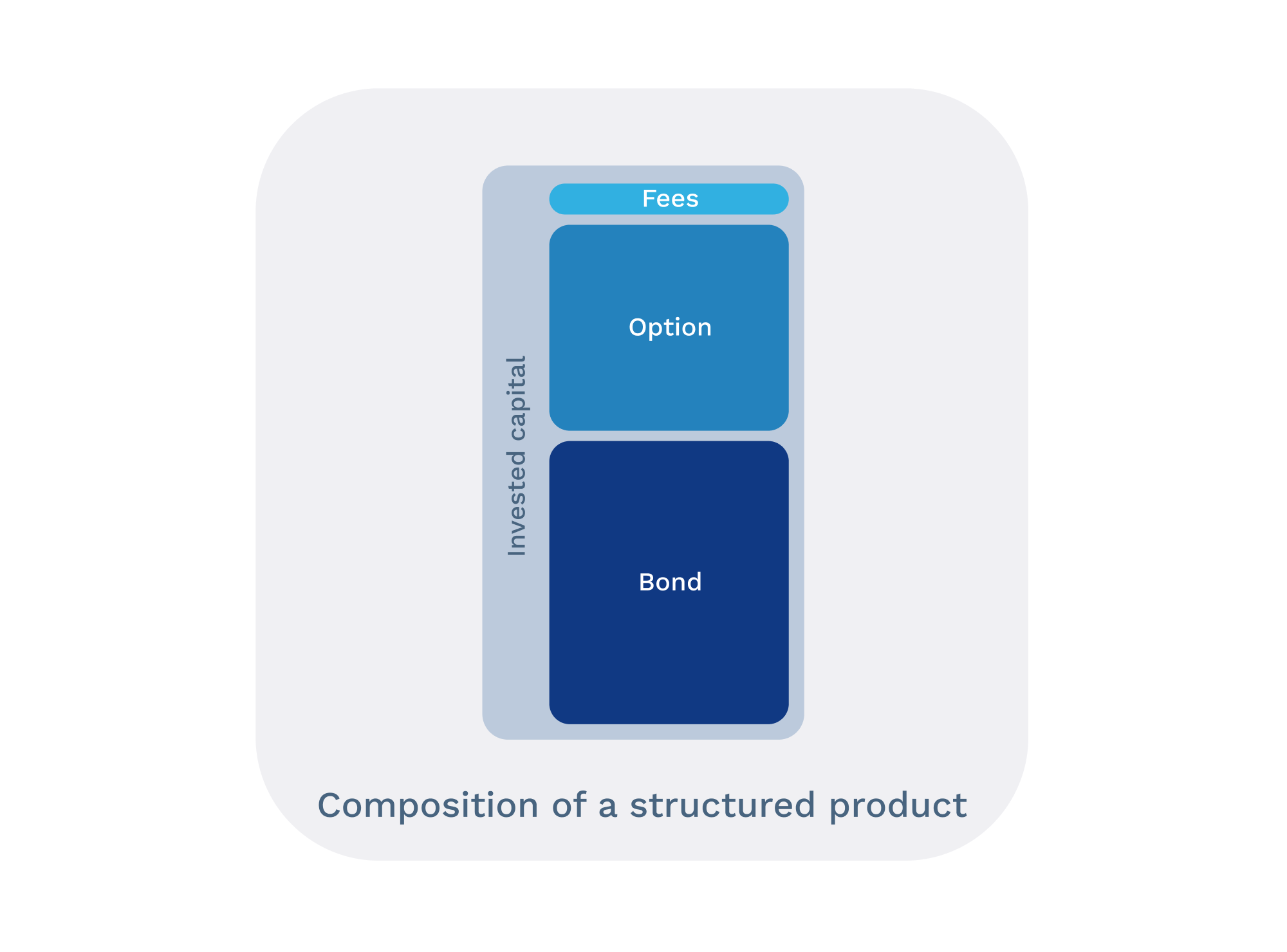

While fees are usually added to the invested amount in most financial products, fees related to structured products are directly integrated into the initial capital and therefore impact the return. For example, if the total fees are 5%, the nominal amount invested in the product will be 95%.

The upfront fee associated with the product is distributed among the marketing participants: distributor, sub-distributor, and the subscription envelope where the structured product will be held (securities account or life insurance contract).

The sensitivity between the offered coupon and the upfront is not linear — raising the upfront by 1% does not equate to a 1% decrease in the coupon (except in the case of a product without early redemption, with a 1-year maturity, offering a guaranteed coupon).

📬 Open offerings

For open offerings — those still being marketed — it is no longer possible to modify the product's features, such as the various barriers, maturity, or offered coupon level. The movements of the underlying asset during the marketing period will only affect the upfront fee. Generally, if the underlying asset's level increases, the upfront fee decreases, and vice versa.

⏱ Amortization

The upfront fee is not deducted directly from the product's value at issuance, preventing a sharp drop in the net asset value due to fees the next day.

It is agreed to smooth out the fees linearly over a predetermined period, which does not exceed the first early redemption date. In the event of significant market increases or to avoid the risk of a client exiting the product too quickly, the fees may be amortized more rapidly to prevent the issuer from suffering a loss on the upfront fee initially paid.

Each client still has the option to manage their amortization according to their preference — generally between 3 and 12 months.

👨⚖️ Regulation

The Monetary and Financial Code stipulates that a Financial Advisor must 'communicate to clients in an appropriate manner the legal nature and extent of [...] information useful for decision-making by these clients, as well as information concerning the terms of their remuneration, including the pricing of their services.' (L.541-8-1).

The MiFID II directive has also reinforced this transparency obligation regarding all fees in a product through a document called the Key Information Document (KID). However, the final investor cannot know the fee distribution among the various participants. Similarly, a Financial Advisor cannot know the fee distribution between the broker and the issuer, unless they use the services of a platform like Feefty, which applies a transparent pricing.

🏃♀️ Running fee

Unlike upfront fees, running fees — or ongoing fees — allow the distributor to be compensated on a recurring basis throughout the product's life. This type of compensation impacts the product's yield, just like the upfront fee. Most Financial Advisors prefer upfront fees, while Life Insurers offering contracts where products are held tend to use running fees as well.

🤓 In summary

The upfront fee refers to the commission amount paid to the distributor(s) and sub-distributor(s) for marketing a structured product. While fees are usually added to the invested amount in most financial products, fees related to structured products are directly integrated into the initial capital and therefore affect the yield. The upfront fee is not deducted directly from the product's value at issuance. Unlike upfront commissions, running commissions—or ongoing fees—allow the distributor to be compensated on a recurring basis throughout the product's life.

Feefty SAS - Capital social 75 000 euros - SIREN 844765578 - RCS Paris - Code APE 6619B - Conseiller en Investissements Financiers - Courtier en assurance - ORIAS n°19001259 orias.fr - Membre de l'AMAFI