The value chain of structured products

The creation of a structured product involves various players, from product structuring — essentially the manufacturing process — to the final subscription by the investor.

🏦 What is an issuer?

An issuer is an entity that issues financial securities. Typically, investment and financing banks issue structured products. A investment bank is a financial institution specialized in market operations, advisory, and intermediation services for other companies. It does not cater to individual clients, a role reserved for commercial or private banks.

Within these banks, several roles contribute to the creation of a structured product. All these roles are typically housed in a trading floor, bringing together different operators:

- Sales are the commercial agents who serve as the bank’s point of contact with clients. Their role is to sell products issued by their bank and to create new products based on client needs. Sales can sometimes create products themselves, but they rely on Structurers for more complex products.

- Structurers, also known as Financial Engineers, specialize in creating all types of products, particularly the more complex ones. They act as a bridge between Sales, who relay client needs, and Traders, who provide directives on parameters like volatility, dividends, etc., that will be used for pricing.

- Traders manage all the products issued by the bank. Their primary role is to hedge positions — also known as exposures — that arise from the issuance of products. They don't speculate on the markets but instead buy and sell various financial assets and derivatives to maintain the initial profit (the margin) until the product’s maturity.

A request for quotation (RFQ) involves seeking pricing from multiple issuers to compare their offers. Although the request concerns the same product, each issuer will quote a different price.

This variance occurs because each issuer has a financial rating that accounts for factors like solvency. The lower the rating, the higher the risk for the investor, and consequently, the more attractive the product's conditions must be—reflecting the risk/return tradeoff.

Another factor to consider is the issuer's need for liquidity, which determines the product’s funding rate. The more urgently a bank needs funds, the higher its funding cost, and consequently, the more attractive the returns it offers.

Lastly, Traders’ assessments of volatility and dividends vary between operators — this is known as marking. Traders must hedge against volatility, and the cost of this hedge depends on their volatility marking. For dividends, a Trader might apply a more or less significant discount relative to the dividends announced by the company whose stock underlies the structured product. The higher the discount, the less attractive the offered coupons will be.

It’s worth noting that some investment banks have developed commercial franchises, particularly in the French market, under different names. The most well-known include Adequity (Société Générale), Privalto (BNP Paribas), Agapan Solutions (Natixis), and Jinko (Crédit Mutuel IM).

Salespeople working within these structures are not intermediaries since they are exclusively tied to a specific bank.

🤝 What is an intermediary?

As the name suggests, an intermediary stands between the issuer and the client. Also known as a distributor, the client is then a sub-distributor before reaching the final investor. The intermediary’s primary role is to conduct an RFQ to compare issuer prices based on the specifications provided by their client. There are different types of intermediaries.

- A broker is the most common type of intermediary. These companies, of varying sizes, offer their clients the ability to conduct the necessary RFQs. They also provide advice and aggressively market their own products to clients.

- A platform is a tool—also known as an application—that offers a neutral approach by allowing clients to browse and purchase the products they want from multiple issuers after an RFQ. The margin is often transparent and fixed for all clients, making it similar to a price comparison tool.

An intermediary cannot offer a better price to a client who requests the same quotation directly from an issuer. One of their added values is that establishing relationships with numerous issuers, and thus obtaining quotations from them, can be complex. Intermediaries grant clients access to trading floors to secure the best possible conditions.

During an RFQ, if the same request reaches a given issuer through two different intermediaries, the investment bank will provide the same quotation to both, regardless of whether intermediary A is a better client than intermediary B or usually conducts a higher volume of business. For the client who requested the RFQ, the only quotation difference will result from the margin policies of the two intermediaries.

💰 Who profits?

All parties involved in the creation of a structured product earn a margin.

The issuer’s margin can be described as soft money. It will only materialize when the product concludes: depending on the positions the Trader took during the product’s creation, this margin may increase or decrease.

Intermediaries earn what is known as hard cash. They take a tangible commission, defined at the product's inception. This commission can take several forms:

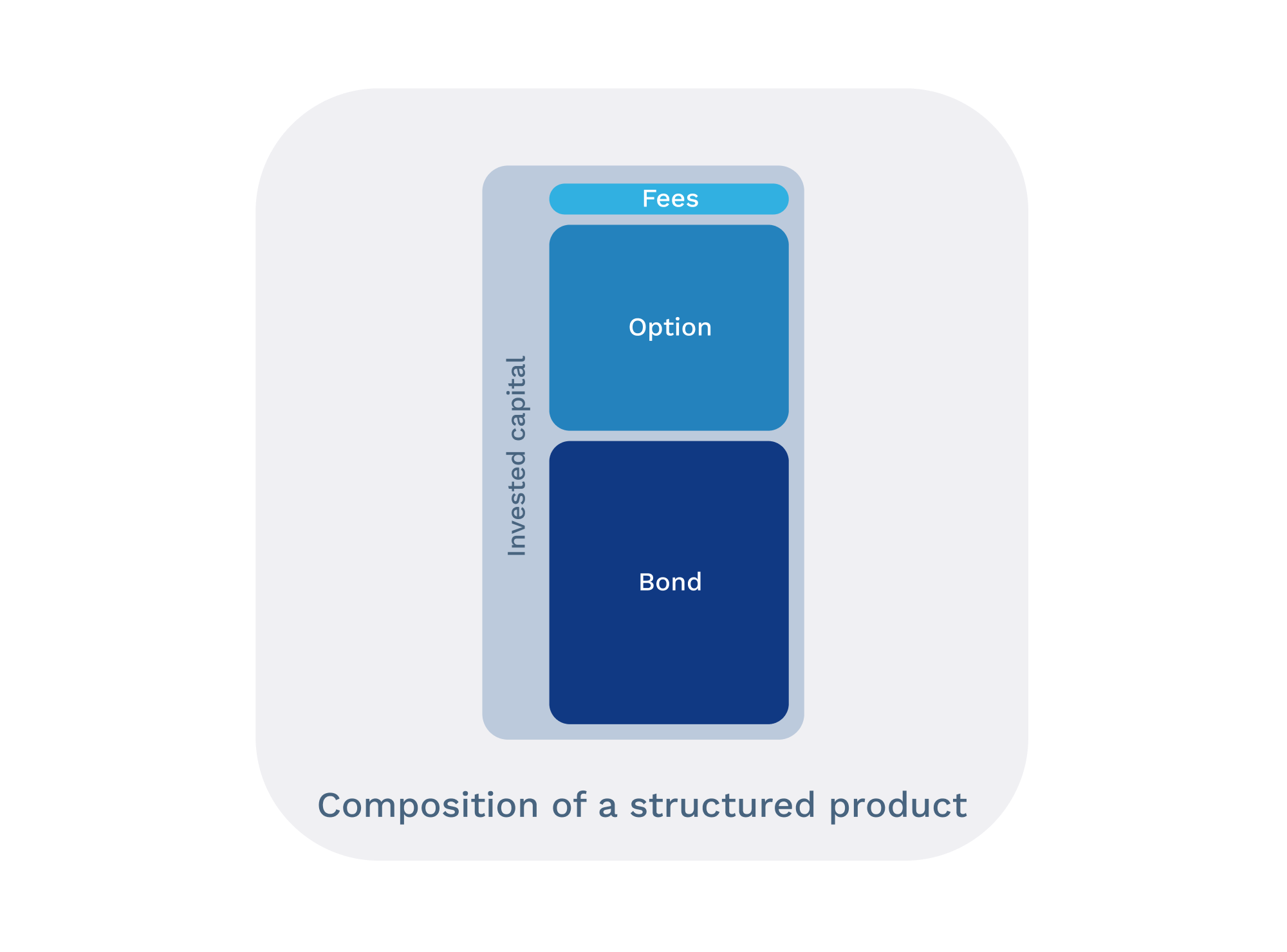

- Upfront refers to the fees charged by the intermediary at the issuance of a structured product. While fees for most financial products are charged in addition to the invested amount, structured product fees are directly integrated into the initial capital, thereby impacting the return. For example, if the total fees are 5%, only 95% of the initial sum will be invested in the product.

- Running fees, like an ongoing commission, allow the intermediary to receive recurring payments throughout the product’s life. For instance, a percentage of the invested amount might be paid every quarter.

🤓 In summary

The creation of a structured product involves various players, from structuring to investor subscription. An issuer is an entity that issues financial securities, typically BFIs that issue structured products. An intermediary stands between the issuer and the client, also known as a distributor, who conducts RFQs to compare issuer prices based on client specifications. All parties involved in creating a structured product earn a margin.

Feefty SAS - Capital social 75 000 euros - SIREN 844765578 - RCS Paris - Code APE 6619B - Conseiller en Investissements Financiers - Courtier en assurance - ORIAS n°19001259 orias.fr - Membre de l'AMAFI