Volatility and structured products: what’s the connection?

🌪 What is volatility?

Volatility is a measure of risk, representing the extent of price fluctuations in a financial asset. The more volatile an underlying asset is, the more likely it is to reach extreme price levels — whether favorable or unfavorable. A riskier underlying asset offers a higher potential return, known as the risk premium. The volatility of stocks typically ranges between 20% and 50%.

Volatility is expressed as a percentage. To simplify, and without considering the time horizon, if an asset's volatility is 5%, the price will fluctuate between -5% and +5% of the underlying asset's average price.

The price of an option consists of its intrinsic value — the difference between the underlying asset's price and the option's strike price — and its time value, which represents the probability of the underlying asset's price change until maturity. Volatility is one of the parameters that affect the option's value. Consequently, the premium of an option increases with the volatility of the underlying asset.

🔎 Historical and implied volatility

There are two ways to measure volatility:

- Historical volatility is based on past data and is calculated as the standard deviation — a measure of value dispersion — of daily price changes;

- Implied volatility is based on the prices of derivatives on the financial asset. It reflects traders' expectations of future price fluctuations. Three factors influence this volatility: the option price, its maturity, and the risk-free rate. Its calculation is based on the Black-Scholes model and the Newton-Raphson algorithm.

⚖️ Option strategies

When an investor buys a stock, they may seek to protect themselves against the stock's volatility — this is known as a hedging strategy. Since there are two types of options — calls and puts — and each type can be bought or sold, there are four possible positions:

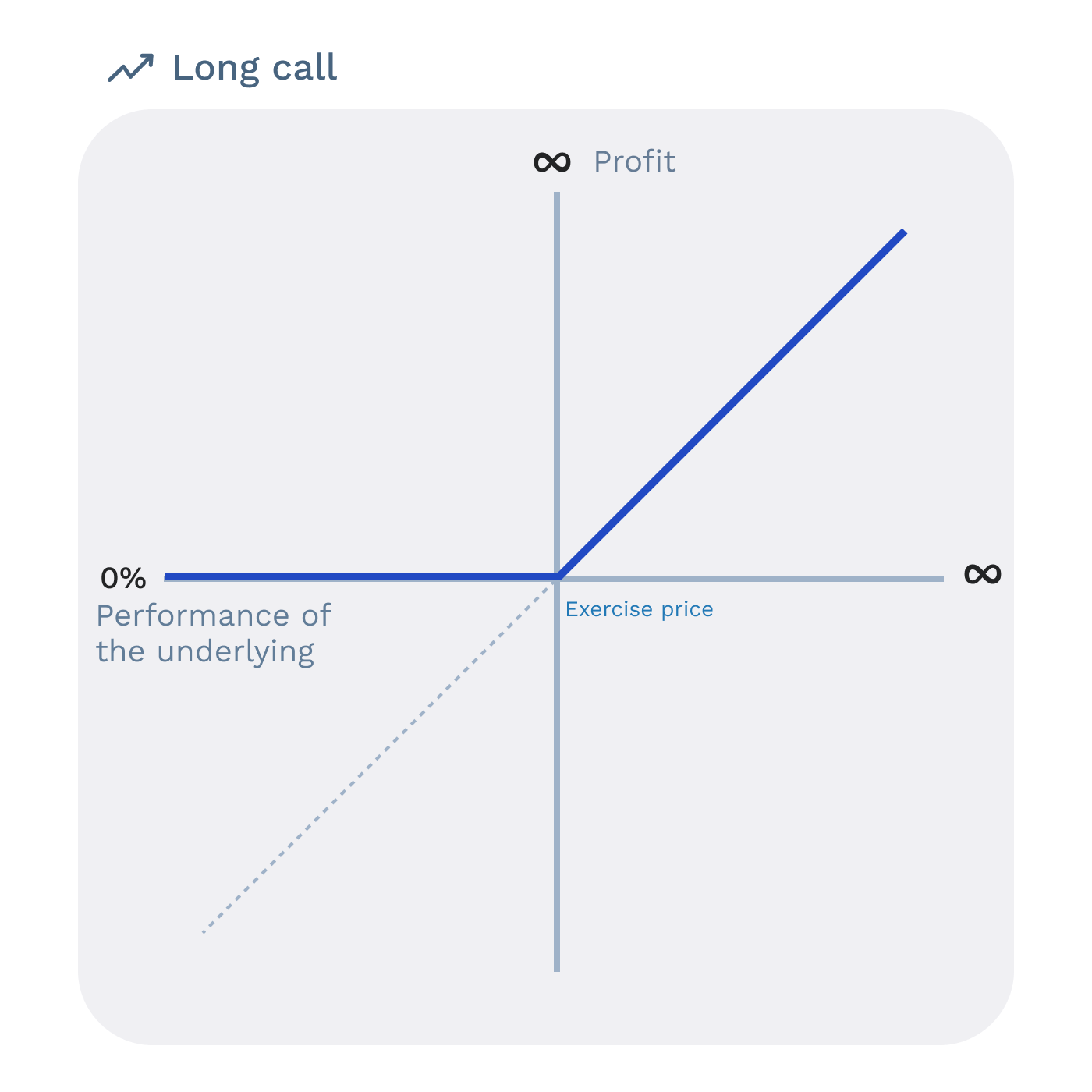

- Long Call (Buying a Call Option): the investor seeks to profit from the underlying asset's rise. At maturity, if the underlying asset's price exceeds the strike price plus the premium, the investor exercises the option and earns the difference. Otherwise, they lose the premium;

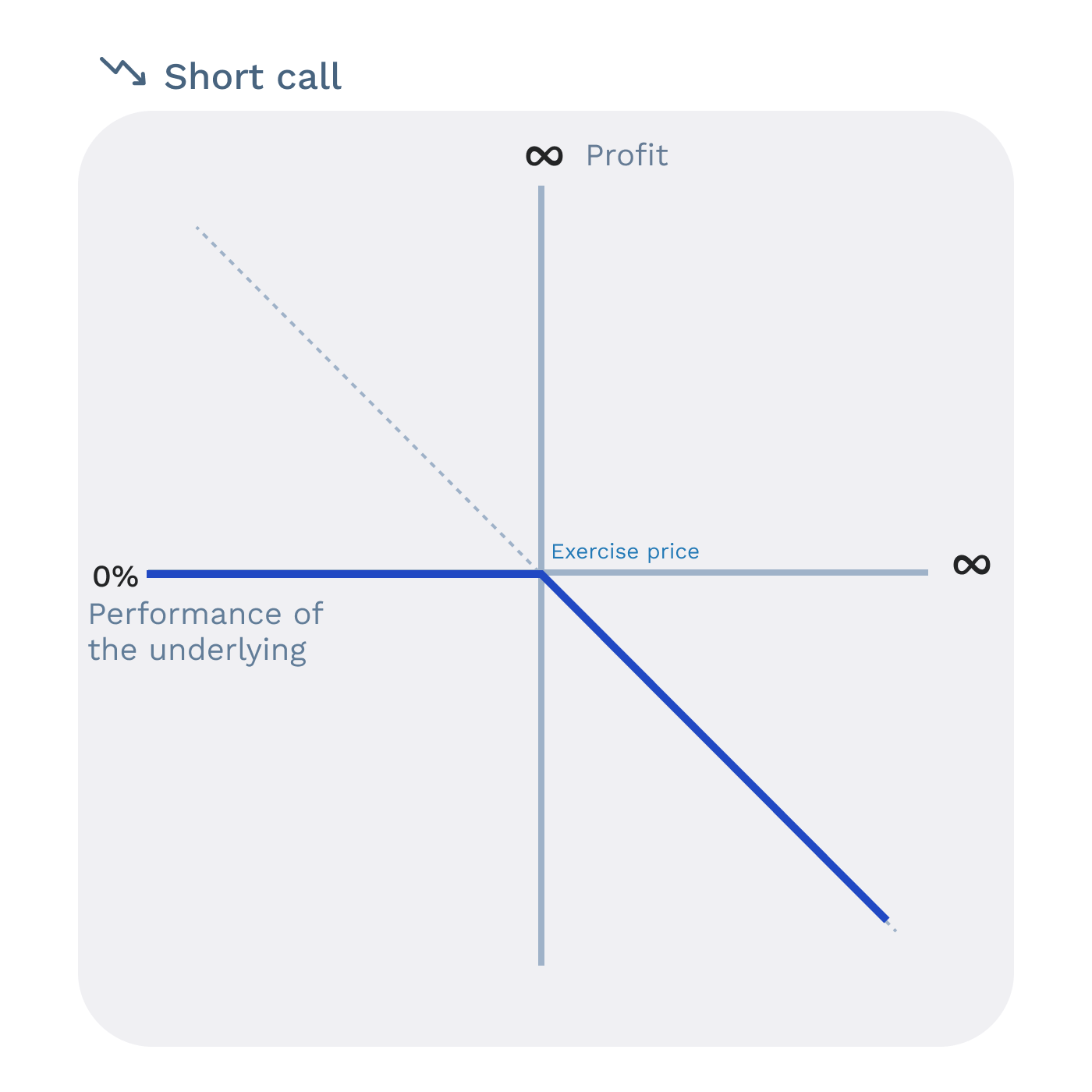

- Short Call (Selling a Call Option): the investor believes the underlying asset will not increase. If the asset's price rises, the seller must buy the stock at a higher price to deliver it at the option's strike price. If it falls, the seller earns the premium. Selling a call option is the riskiest position since the asset's price can rise indefinitely;

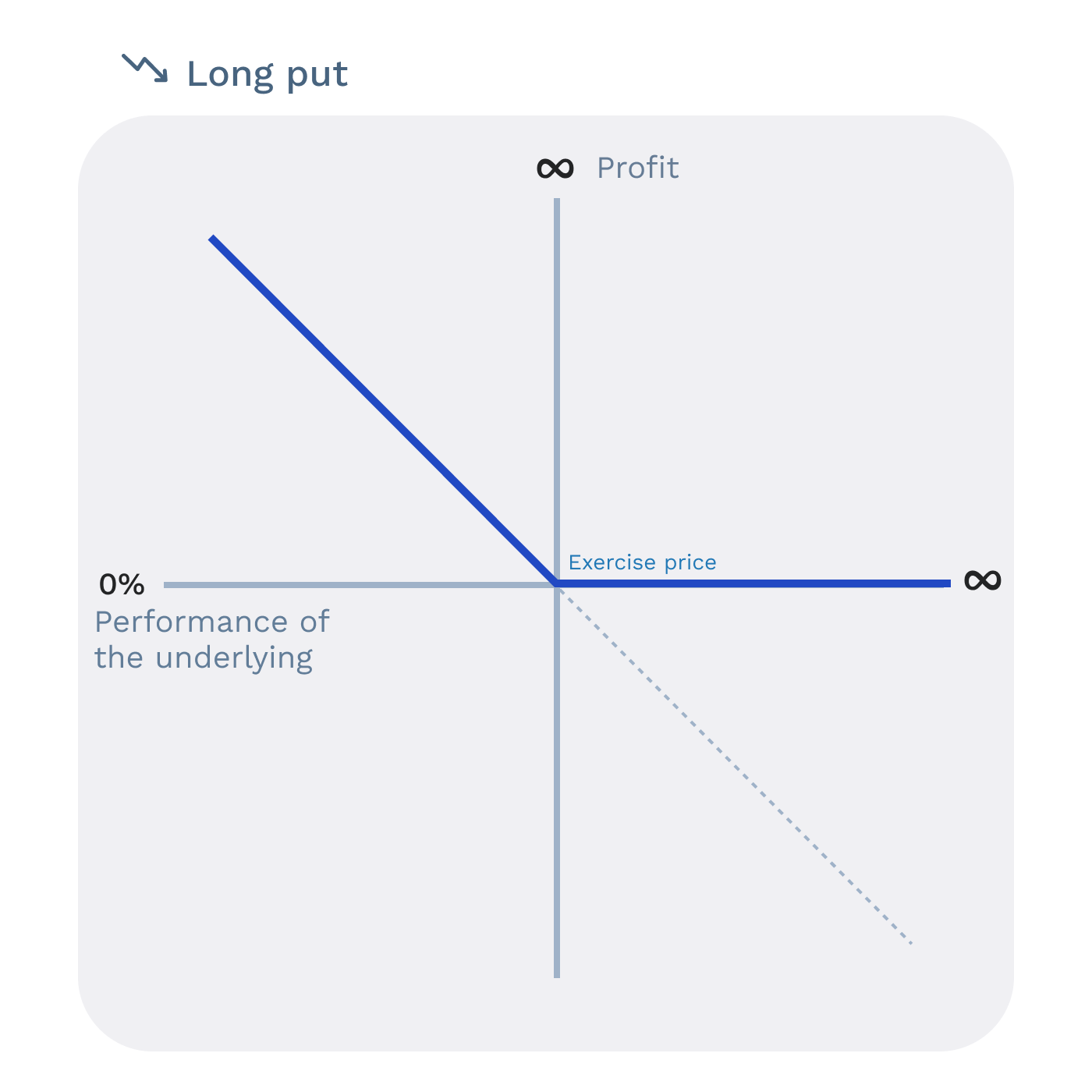

- Long Put (Buying a Put Option): the investor seeks to hedge against a drop in the underlying asset's price. If the drop occurs, they can sell the asset at the strike price. Otherwise, they lose the premium;

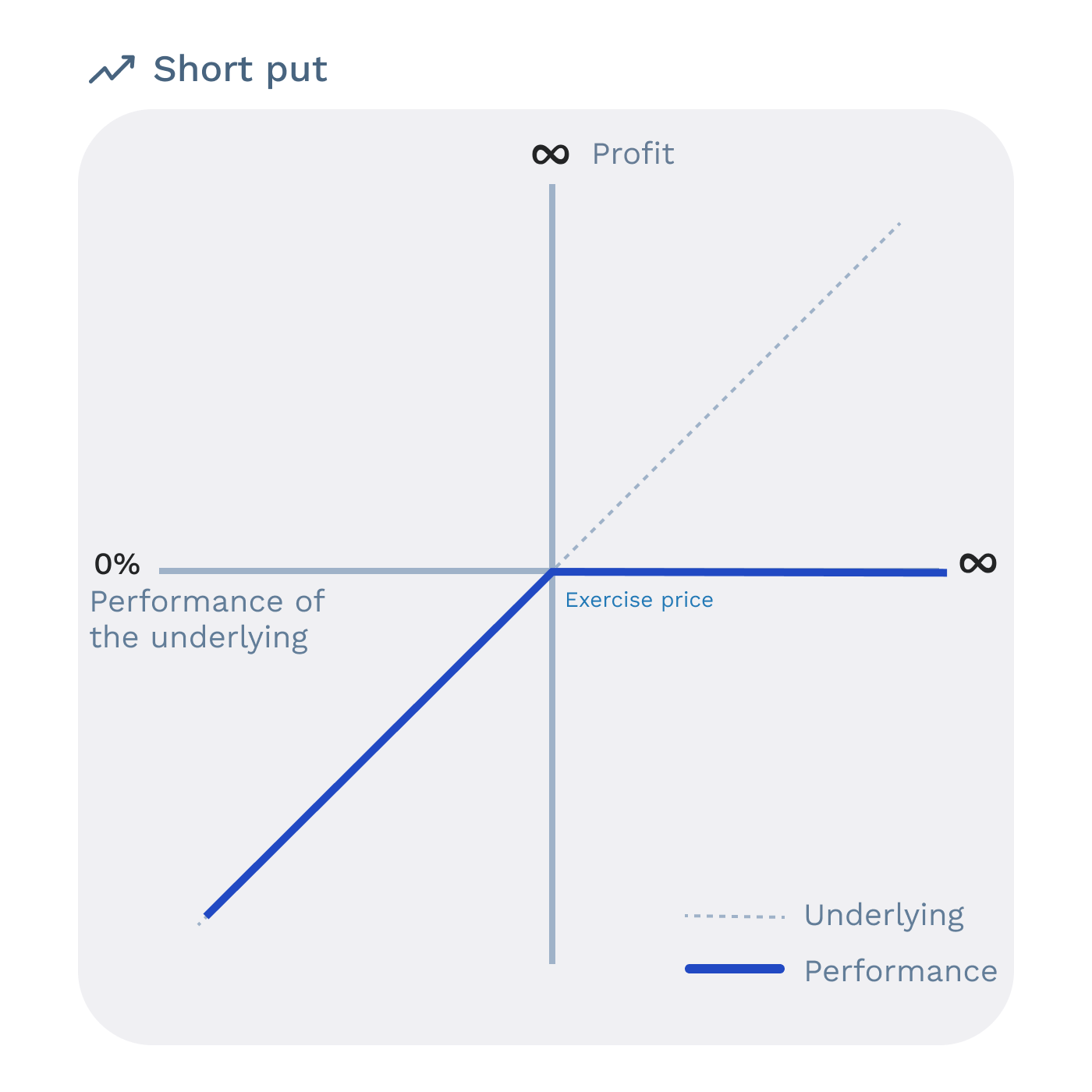

- Short Put (Selling a Put Option): the investor anticipates that the underlying asset will not decrease. If correct, they earn the premium. Otherwise, they must buy the underlying asset at a price higher than their sale commitment.

* These charts do not include the option premium.

😲 The VIX or fear Index

The VIX (Volatility Index) is an indicator of the volatility of the U.S. market. It averages the annual volatilities of call and put options on the S&P 500 index. For example, if investors anticipate a market decline, they will buy put options on the S&P 500 to hedge themselves. As investors' anxiety increases, so does the demand for put options. Since buying options equates to buying volatility, this increased demand leads to a rise in the VIX, earning it the nickname "the fear index."

📈 And for structured products?

Since an option's value is the sum of its intrinsic value and time value, selling an option equates to selling volatility. When volatility increases, the option's value also increases, resulting in a higher potential return.

In most structured products (Autocall, Phoenix, Reverse, etc.), the investor is selling a put option — thus selling volatility. They anticipate stability or an increase in the underlying asset's price. In a volatile context, this option becomes more valuable, mechanically offering a higher potential return — the coupon — on the product.

The structured product issuer — a bank — will hedge against this position initiated by the investor. The trader will buy and sell various financial assets and derivatives to maintain the initial gain made on the transaction until the product's maturity.

🤓 In summary

Volatility is a measure of risk, representing the extent of price fluctuations in a financial asset. There are two ways to measure volatility: historical and implied volatility. When an investor buys a stock, they seek to hedge against the stock's volatility—known as a hedging strategy. Since there are two types of options—calls and puts—and each type can be bought or sold, there are four possible positions. An option's value consists of its intrinsic and time value, and its value is positively influenced by volatility. A structured product contains an options component, so if volatility increases, the offered coupon will also increase.

- Useful links

- About

- Resources

- Glossary

- Browse products

Feefty SAS - Share capital 75 000 euros - SIREN 844765578 - RCS Paris - APE code 6619B - Financial Investment Advisor - Insurance Broker - ORIAS n°19001259 orias.fr - Member of AMAFI