What are the different types of capital protection?

Finance is often said to be reserved to an elite. As if it had be complex to be credible. The jargon only makes it worse, widening the gap between those in the know and those who aren't.

We will attempt to simplify our approach by classifying and translating these terms.

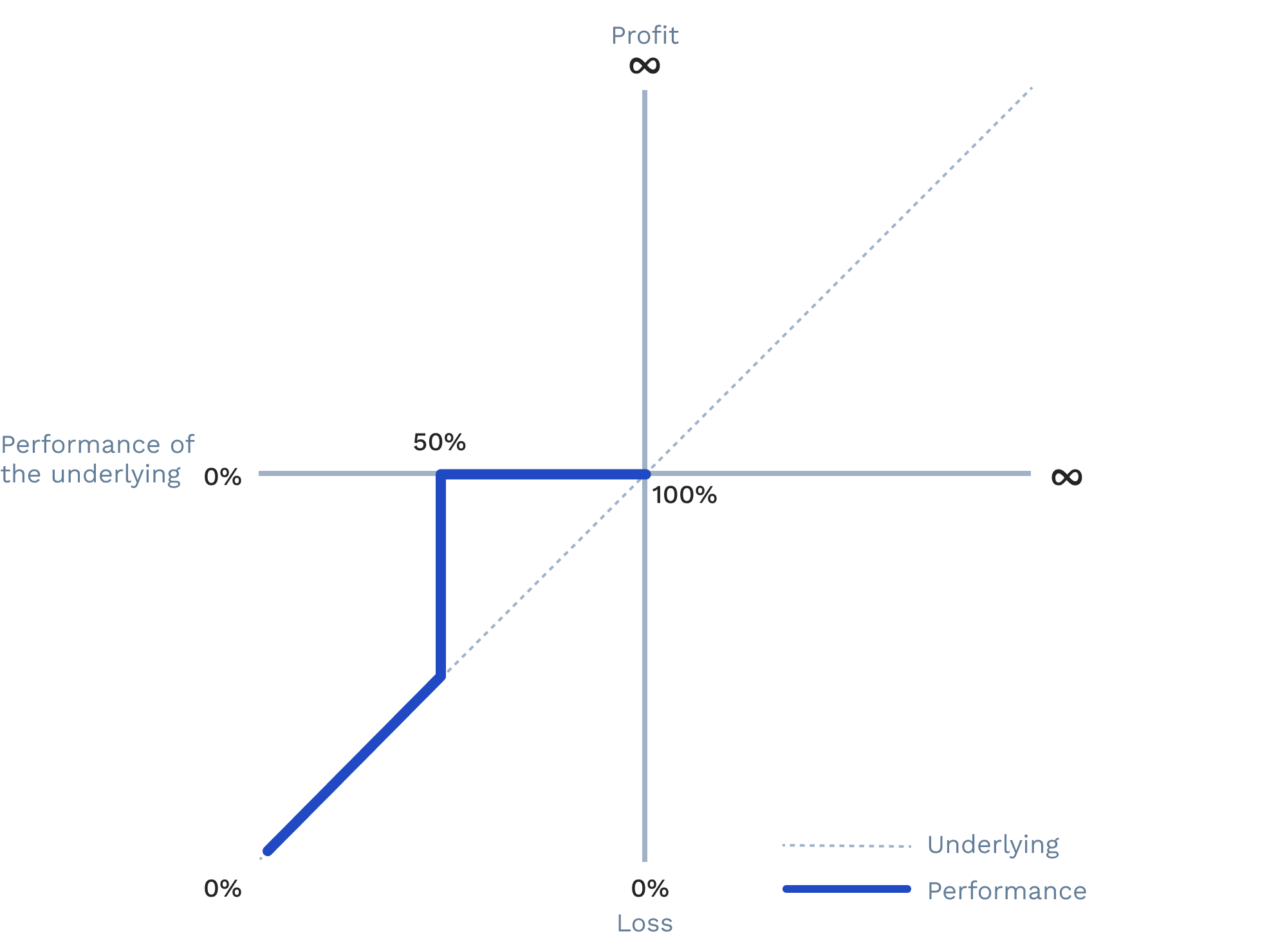

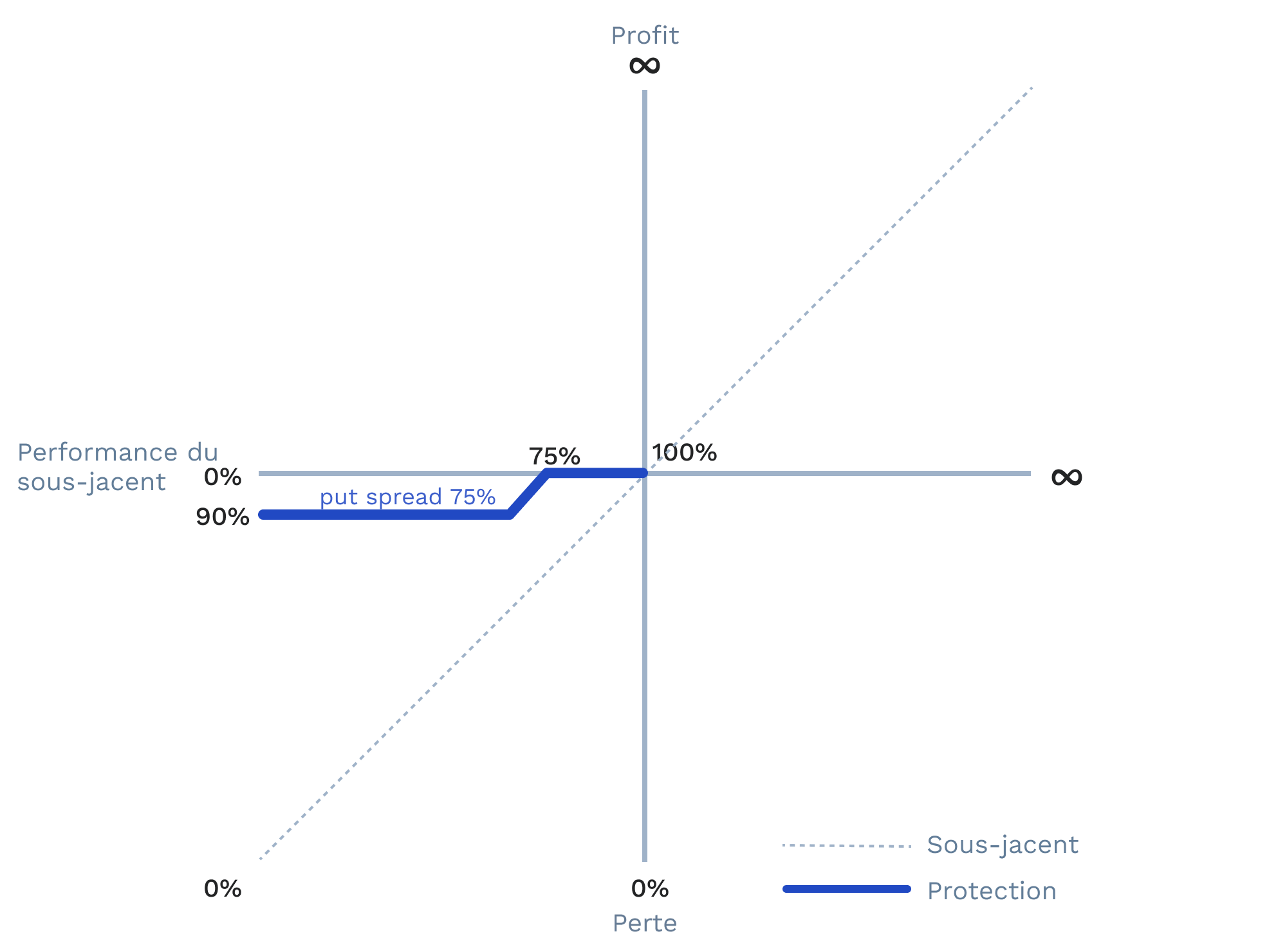

🚧 Protection Barrier

The barrier refers to the image of breaching through something, which leads to a fall from the level of the barrier. In the case of a protection barrier set at -50% compared to the initial level (Strike), if the underlying asset is observed at -55%, the capital loss will not be 5% but 55%. The investor will be refunded 45% of their initially invested amount.

This is also called a Put Down & In or Knock-In Barrier.

This is the most common type of protection. It offers the least security and therefore the highest return (Return/Risk).

EXAMPLE

In the case of a European barrier at -50%, if at maturity the underlying asset has not fallen by more than 50%, the capital is protected.

If the underlying asset's performance reaches -51%, the amount refunded will be 49% of the initially invested capital. The capital protection at maturity is therefore highly sensitive to a slight variation in the underlying asset around the barrier threshold.

There are several types of barrier:

- At maturity: called a European barrier, the performance of the underlying asset is only observed at maturity. This is the most commonly used type of protection.

- Continuous: called a continuous American barrier, the performance of the underlying asset is observed without interruption throughout the product's life.

- At close: called a closing American barrier, the performance of the underlying asset is observed at each closing price.

In the case of American barriers, once the barrier is breached, it no longer exists. This protection is commonly used on the Swiss market.

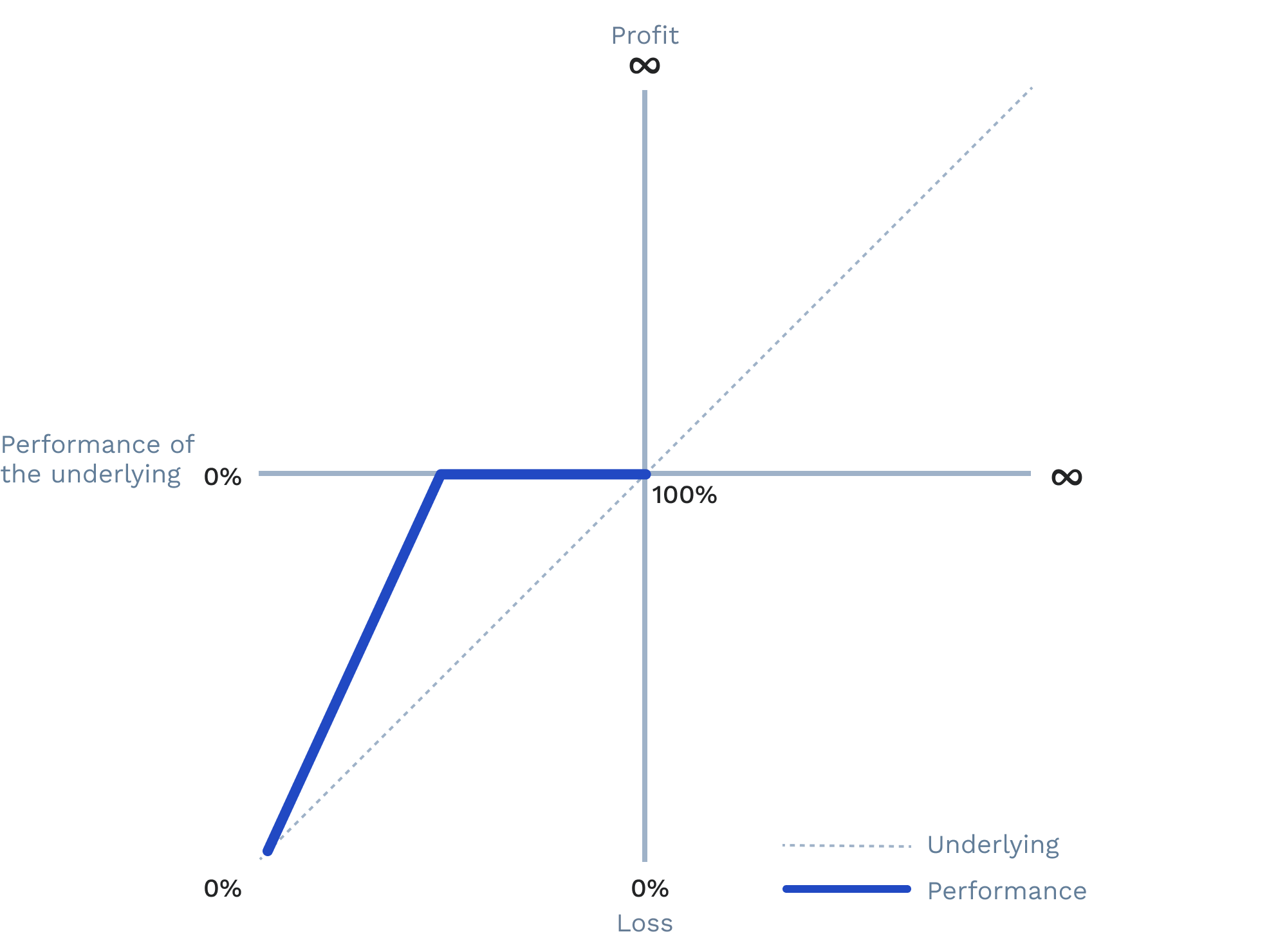

⛷️ Leveraged protection

This refers to an accelerating effect. Leverage generally means a multiplier greater than 1. To calculate leverage, we simply divide 100% (reference base) by the level of protection in absolute value: with protection at 50%, the leverage equals 100% / 50%, or 2 — so 200%.

Thus, in the case of -50% leveraged protection, if the underlying asset is observed at -55% — so 5% below — the capital loss will be 10%. The investor will be refunded 90% of their initially invested amount.

This is also called Low Strike, Put Leveraged or Geared Put.

This is an intermediate type of protection between the barrier and simple protection.

EXAMPLE

In the case of -50% leveraged protection, the capital loss will be 2% for each percentage point drop below the protection level.

If the underlying asset's performance is above -50% of the initial level, the capital is protected.

If the underlying asset's final performance is -51%, the investor will suffer a capital loss of 2% and will be refunded 98% of their initially invested capital.

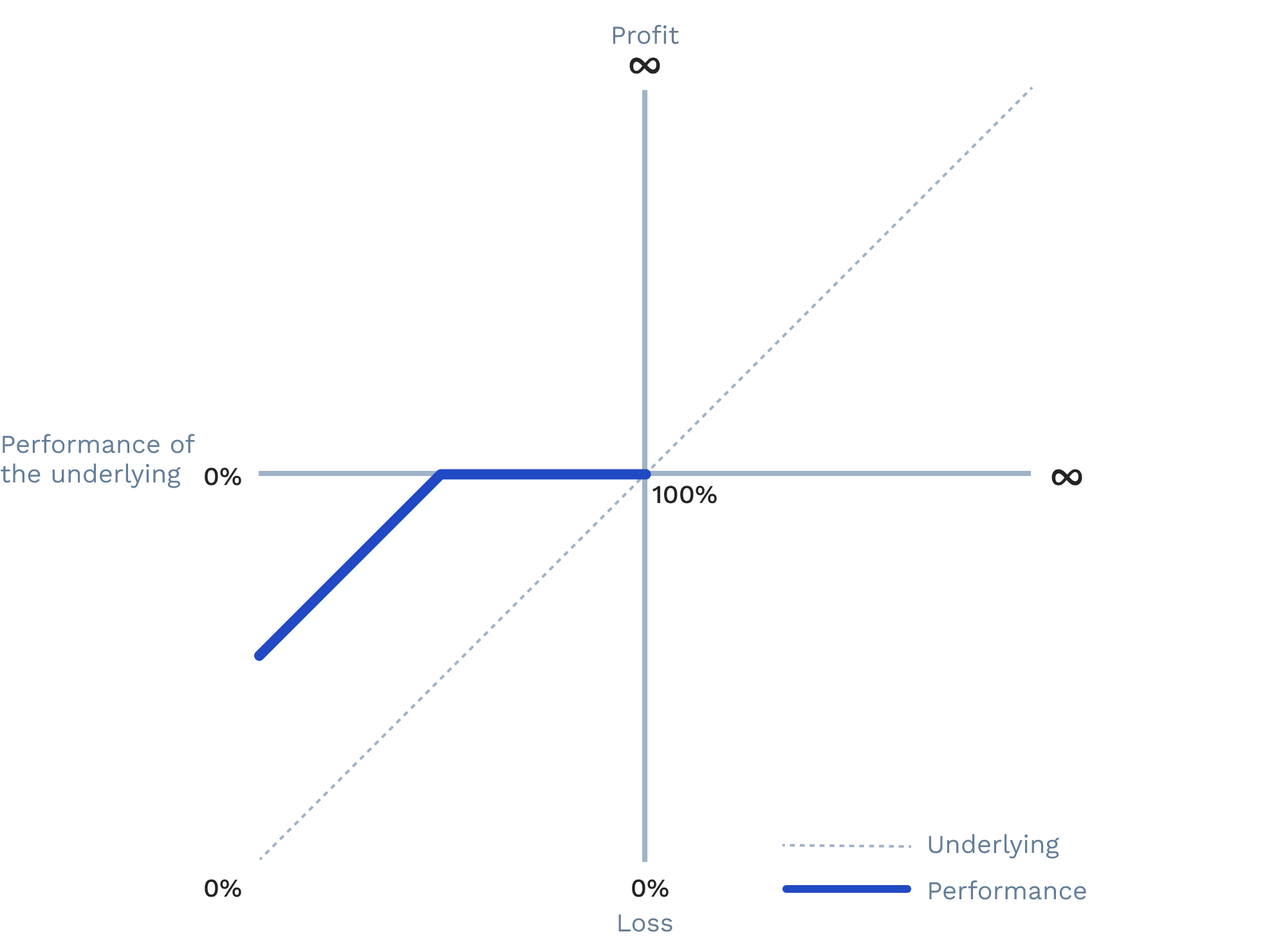

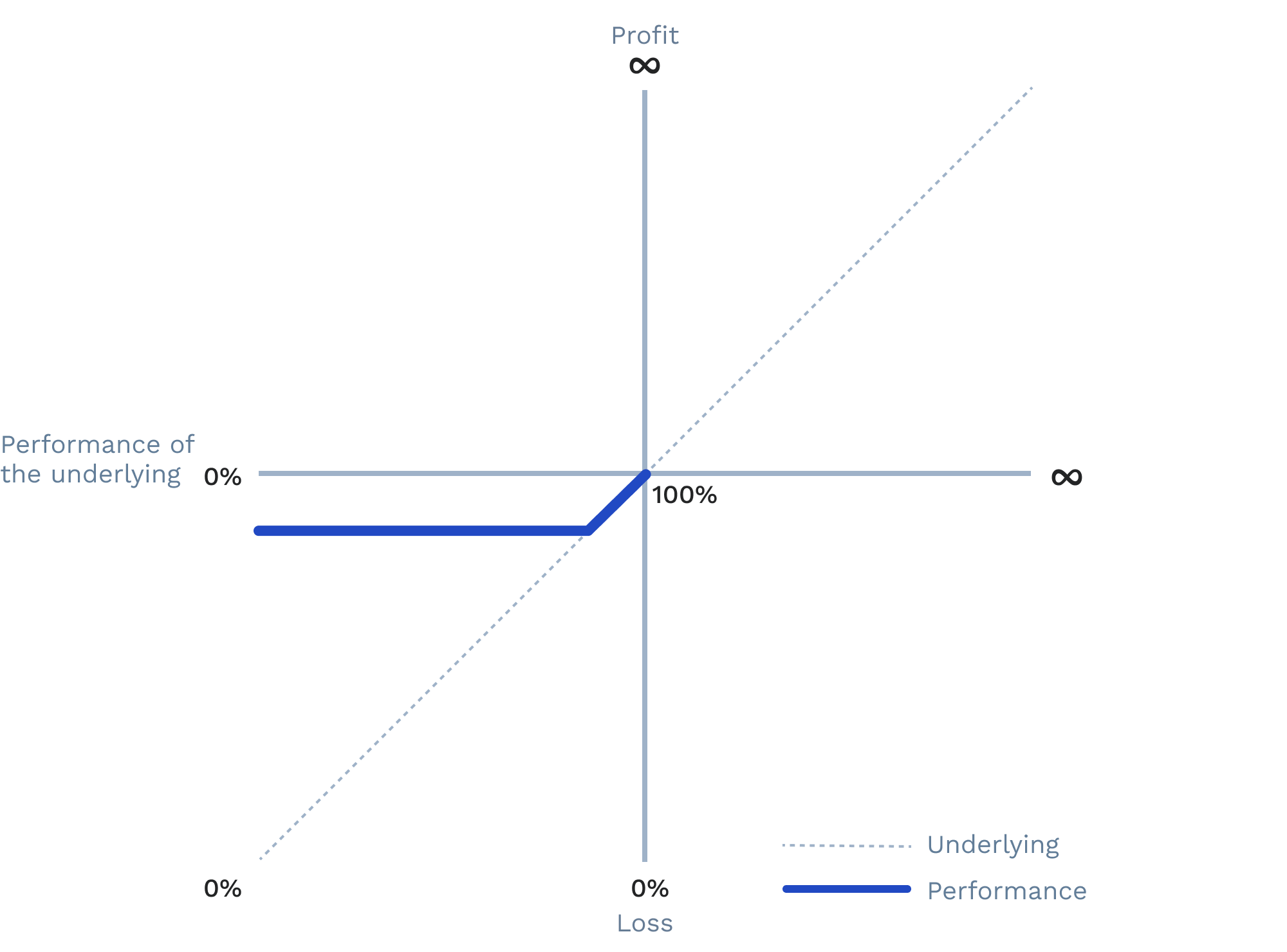

🦺 Simple protection

This one is straightforward. It is a protection that, if the condition is not met, leads to a capital loss equal to the drop in the underlying asset below this level.

In the case of simple protection at -50% compared to the initial level (Strike), if the underlying asset is observed at -55% — so 5% below — the capital loss will be 5%. The investor will be refunded 95% of their initially invested amount.

This is also called Vanilla Put or Put.

This protection is less risky than the previous ones, and therefore less rewarding.

EXAMPLE

In the case of simple protection at -50%, if the underlying asset's final performance is above -50% of the initial level, the capital is protected.

If the underlying asset's final performance reaches -51%, the investor will suffer a capital loss of 1% and will be refunded 99% of their initially invested capital.

In other words, in this example, the capital is guaranteed up to 50%.

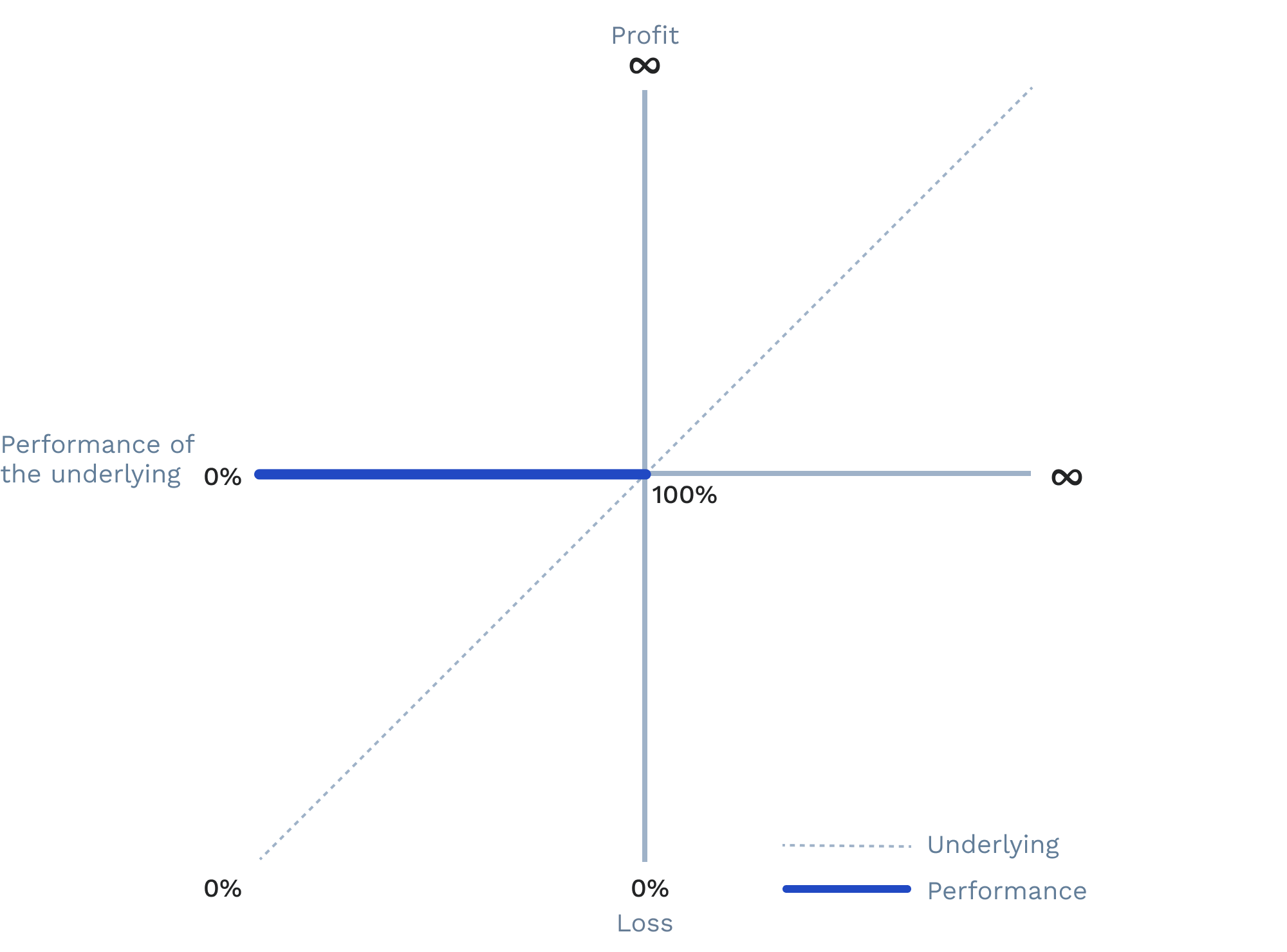

🛡️ Guaranteed capital

It is important to first note that Guaranteed Capital is understood to be conditional to the issuer's default. The term guarantee refers to something solid and reassuring. There are 2 types of guarantees: total guarantee and partial guarantee. Total guarantee is associated with the 100% level (reference base), while partial guarantee is associated with a lower level, for example, 90%.

In the case of a 100% guaranteed capital compared to the initial level (Strike), regardless of the level at which the underlying asset is observed, the investor will not suffer any capital loss. They will be refunded 100% of their initially invested amount.

This is also called Full Principal Protection, guaranteed capital, or abbreviated as KG.

With this protection, the capital is guaranteed regardless of the underlying asset's final performance. It offers very little risk and is not highly rewarding.

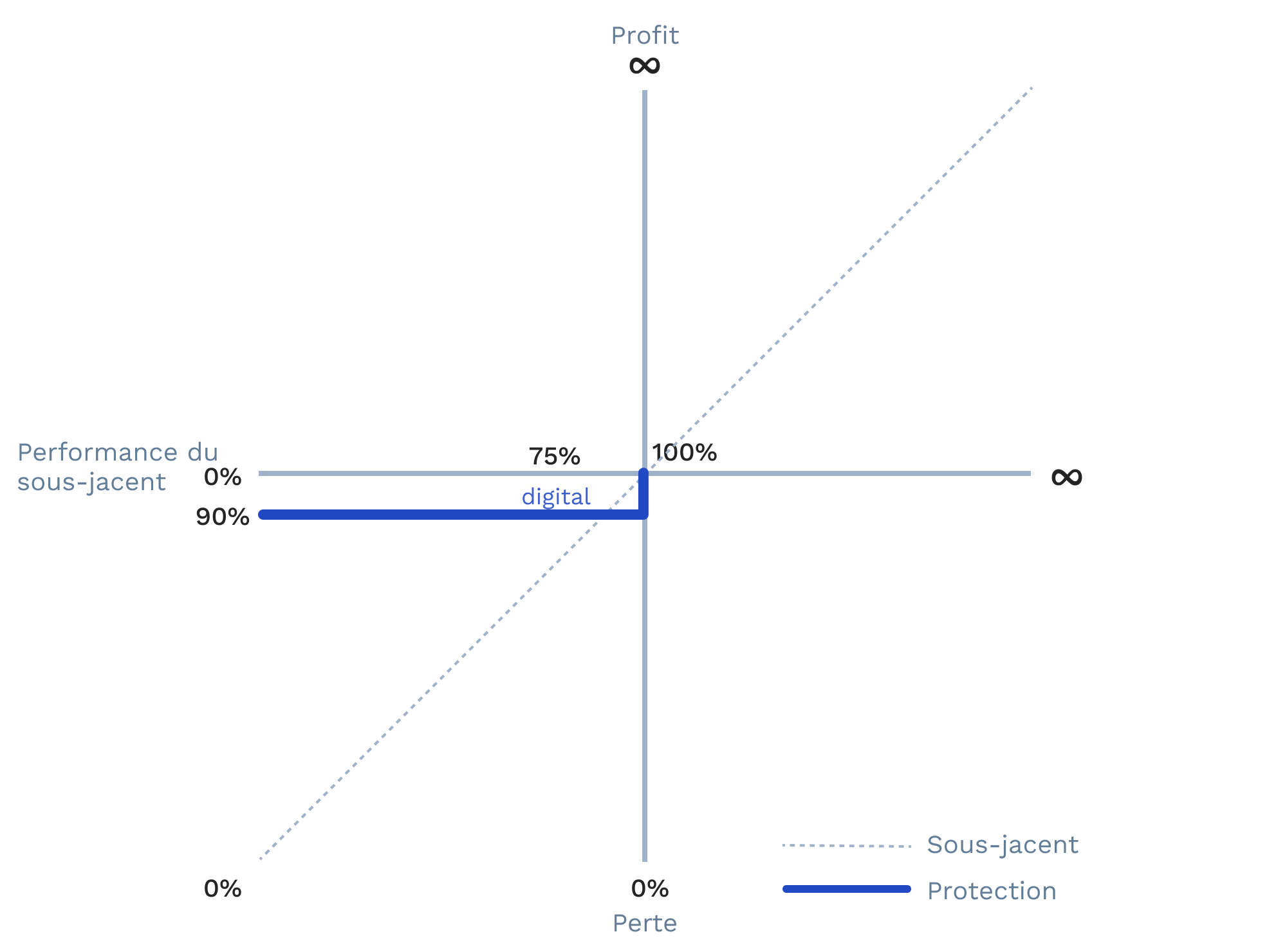

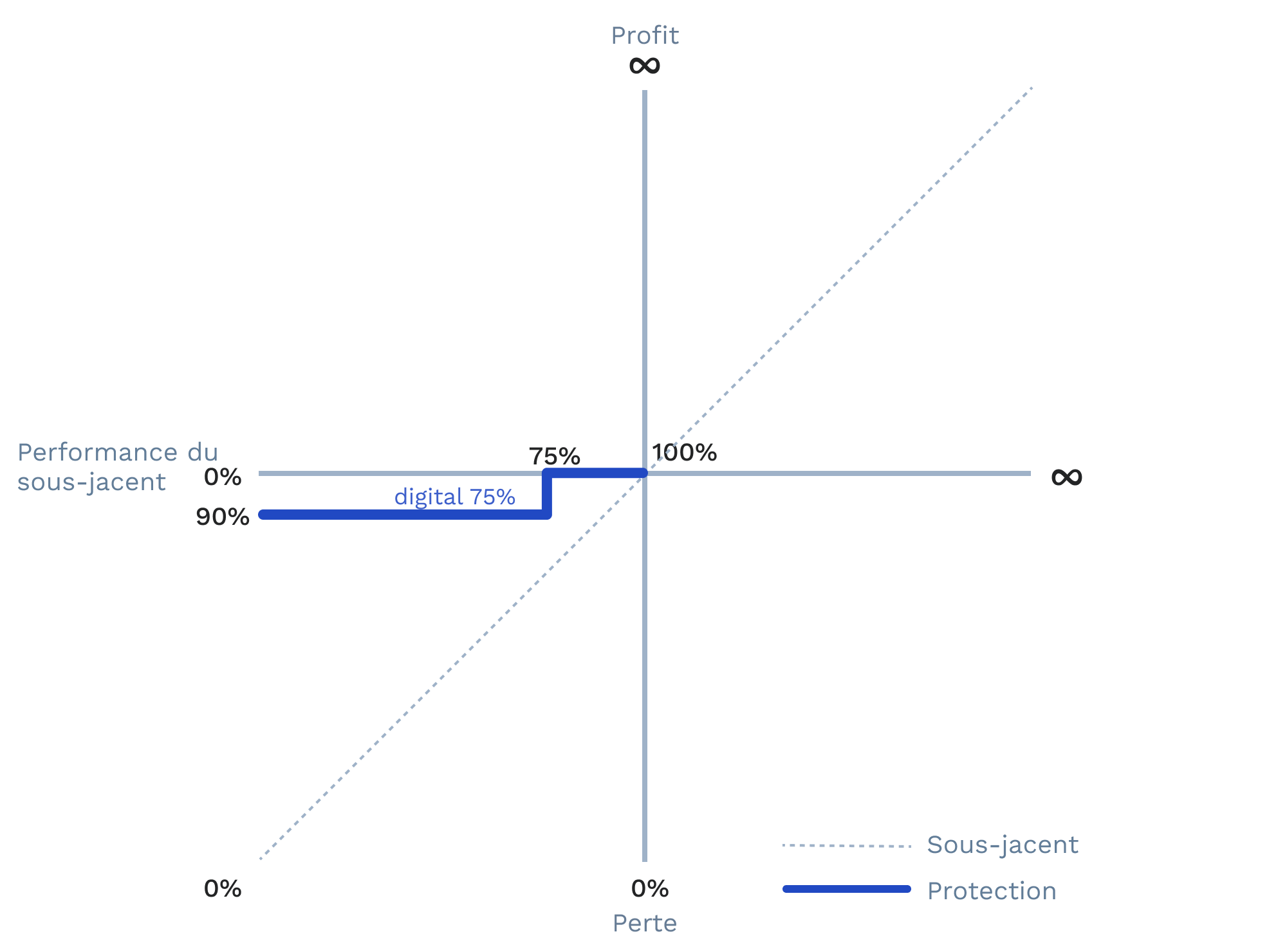

🛡️ Partially guaranteed

Here too, the guarantee is subject to the default of the issuer. In the case of a partial guarantee at 90% compared to the initial level, if the underlying asset is observed below 90%, regardless of the level, the investor will suffer a capital loss of no more than 10%. They will therefore be refunded 90% of their initially invested amount.

This is also called Partial Principal Protection, X% guaranteed capital, or abbreviated as x% KG.

Partial guarantee can also be associated with other types of protection, to only benefit from the drop after a certain threshold or to have a barrier instead of a progressive drop.

- Useful links

- About

- Resources

- Glossary

- Browse products

Feefty SAS - Share capital 75 000 euros - SIREN 844765578 - RCS Paris - APE code 6619B - Financial Investment Advisor - Insurance Broker - ORIAS n°19001259 orias.fr - Member of AMAFI